As I found out as part of our Caravan Guard interview, caravan insurance premiums can range anywhere from £90 to over £500 depending on the value of your tourer. If your caravan insurance seems a little on the high side, you might be wondering if there are some ways that you can reduce your insurance premium.

Here are a few actionable tips for reducing your caravan insurance premium, based upon my research:

- Store your caravan in a CaSSOA-approved leisure vehicle storage site

- Pay your premium in full rather than in little chunks

- Carefully choose the appropriate policy type for you

- Join a national caravan club for access to their discounted insurance products

- Actually work out the value of your contents, rather than just estimating

- Fit your caravan with more anti-theft devices, such as a tracker

- Check the value of your caravan rather than estimating

I believe these are tips that everyone can benefit from and they will genuinely save you money when it comes to arranging insurance for your tourer. I’m going to talk through each tip in a little more detail.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

Store your caravan in a CaSSOA-approved leisure vehicle storage site

One thing in particular that has a big impact on your caravan premium is where you’re going to store it.

Think about it this way. If you’re storing your caravan on the side of the road or a drive that isn’t gated off, it’s more likely to be damaged or stolen versus storing it in a secure facility.

So where, ideally, should you store your caravan?

All caravan owners should store their caravan in a CaSSOA-approved leisure vehicle storage site, as this can reduce your insurance premium significantly versus storing your caravan elsewhere such as your drive at home.

What’s a CaSSOA-approved site?

CaSSOA stands for Caravan Store Site Owners’ Association. CaSSOA represents caravan storage site owners across the UK. However, leisure vehicle storage site owners must meet a strict criteria to be approved by CaSSOA and awarded one of their 3 accreditations.

The more secure a storage site, the greater the accreditation it is awarded by CaSSOA. Caravan insurers notably appreciate when a caravan owner stores their tourer on a CaSSOA-approved site.

Insurers recognise that CaSSOA takes security very seriously and regularly reviews registered sites to ensure they’re still worthy of accreditation. Therefore this can bring your insurance premium down if your caravan is stored on one of these sites.

To find out more about CaSSOA-approved sites and how members gain accreditations, please click here to read my blog post about it.

Pay your premium in full rather than little chunks

This might seem a little obvious but I thought it was worth mentioning anyway. You can pay your premium in one payment rather than paying monthly and this will reduce the amount you pay overall.

If you choose to pay your caravan insurance in monthly payments, the finance company working in coordination with insurer pays the full fee upfront. You’re essentially paying the finance company back over the course of the year.

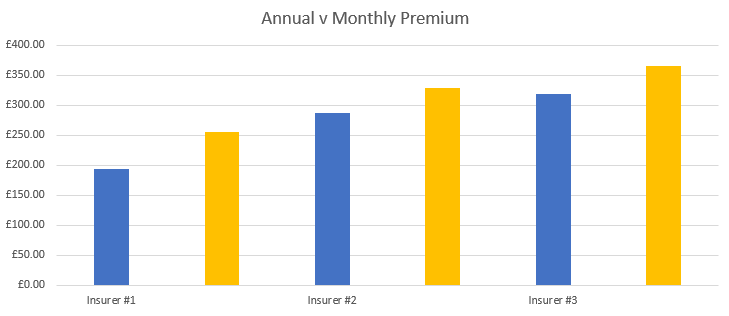

The finance company adds interest rates to your premium. This means you can end up spending significantly more. To demonstrate this, I went away to get some insurance quotes for my tourer to see how different the premium was when paying upfront versus paying monthly.

As you can see on the graph above, paying your caravan insurance in one payment makes sense. If you pay in monthly payments (yellow columns), you end up paying more.

With Insurer #1, the one-off annual payment is £193.33. If you choose to pay in 12 monthly payments, the premium is £255.24.

As the graph shows, it’s a similar story regardless of which insurance provider you choose.

While paying your insurance premium annually might cause some short-term cash flow problems, it makes sense to do so when you look at the bigger picture.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

Carefully choose the appropriate cover type for you

Carefully choosing the cover type can help you to reduce your insurance premium.

There are two primary cover types for caravans:

- New for Old

- Market Value

These two types of cover are very different.

New for Old caravan cover provides you with a brand new equivalent of your tourer in the event of a total loss claim.

Market Value caravan cover means you’ll be paid out whatever amount your caravan is currently worth at the time of loss.

Depending on the age and current value of your caravan, these cover types can differ greatly in price.

If your caravan is brand new, there won’t be much difference in price between New for Old and Market Value cover. On the other hand, if your caravan is a more than 3 – 4 years old, the insurance premium can differ greatly depending on the cover type you choose.

Decide carefully whether you need New for Old or Market Value cover, because the costs will be astronomically different if you have an older caravan.

Join a national caravan club for access to their discounted insurance products

One way of reducing your caravan insurance premium is joining a national caravan club and utilising the insurance policies they offer.

The Caravan and Motorhome Club and The Camping and Caravanning Club both offer access to member-only insurance products.

The insurance products available via either of the big national clubs are often cheaper than those you’ll find elsewhere on comparison sites.

Of course, signing up to either of the two big national caravan clubs gives you a host of benefits. Both offer excellent insurance products, but each offer unique benefits. I wrote a blog post, Which Caravan Club Is The Best? Which can help you to determine which of the two clubs is best for you. It’s well worth a read if you can’t decide!

Actually work out the value of your contents rather than estimating

When you’re getting caravan insurance quotes, you’ll be asked something along the lines of “what is the total value of personal effects in the caravan?” or “what is the total value of equipment in the caravan?” In fact, some insurers will ask both questions.

Something I’m personally guilty of is just guessing the answers to these questions. Estimating is so much easier than going away and working out the actual answer to both questions. It is worthwhile finding out the actual value of the personal effects and equipment in your caravan, however.

The answers to these questions will affect your insurance premium. If you estimate too highly, you could be paying more than you have to.

Take the time to work out the value of your personal effects (items you have brought from home such as clothes and bed linen) and equipment (such as heaters and electrical equipment) and you could end up saving a lot of money on your premium.

Fit your caravan with anti-theft devices such as a tracker

Caravan insurers obviously consider security very important. If your caravan isn’t secure, it increases the chances of something happening to it. You end up paying more because the risk is increased for your insurer.

You can therefore reduce your caravan premium by fitting anti-theft devices to it and increasing how secure it is.

There are a number of devices that you can fit to your caravan, such as:

- Alarm

- Tracking device

- Wheel clamp

- Hitchlock

- Axle wheel locking device

- Security tagging

- Security post

- Locking wheel nuts

It’s worthwhile having a look at all of the above security measures, because they may reduce your insurance premium. A good idea to determine what you should invest in is to go to a insurance comparison site, select the devices one by one, and see how much they bring the insurance premium down. Then you can determine which you are best investing in.

Check the value of your caravan rather than estimating

This tip really only applies for those going to Market Value cover but it’s worth keeping in mind regardless of what cover type you decide on.

Similar to the tip regarding your equipment and personal effects, actually find out the market value of your caravan rather than just estimating. If you estimate too much, you simply end up paying more than you really should be.

Get an accurate market value for your caravan and you pay exactly what you should be for the cover you need.

That wraps up my 7 tips for reducing your caravan insurance premium. Please take the time to have a look at the other resources I’ve linked to throughout this blog post if you’re wanting to learn more about caravan insurance and save some money.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

Here are some other blogs I’ve written that are particularly worth a read if you’re sorting insurance for your caravan now.