As a caravan lover, I’ve discussed every aspect of caravanning with fellow caravanners — even caravan insurance! A question that crops up time and time again — particularly with people considering the purchase of their first tourer — is what does caravan insurance cover? I decided to write a blog post and fully answer this question with a little bit of help from a few caravan insurance experts.

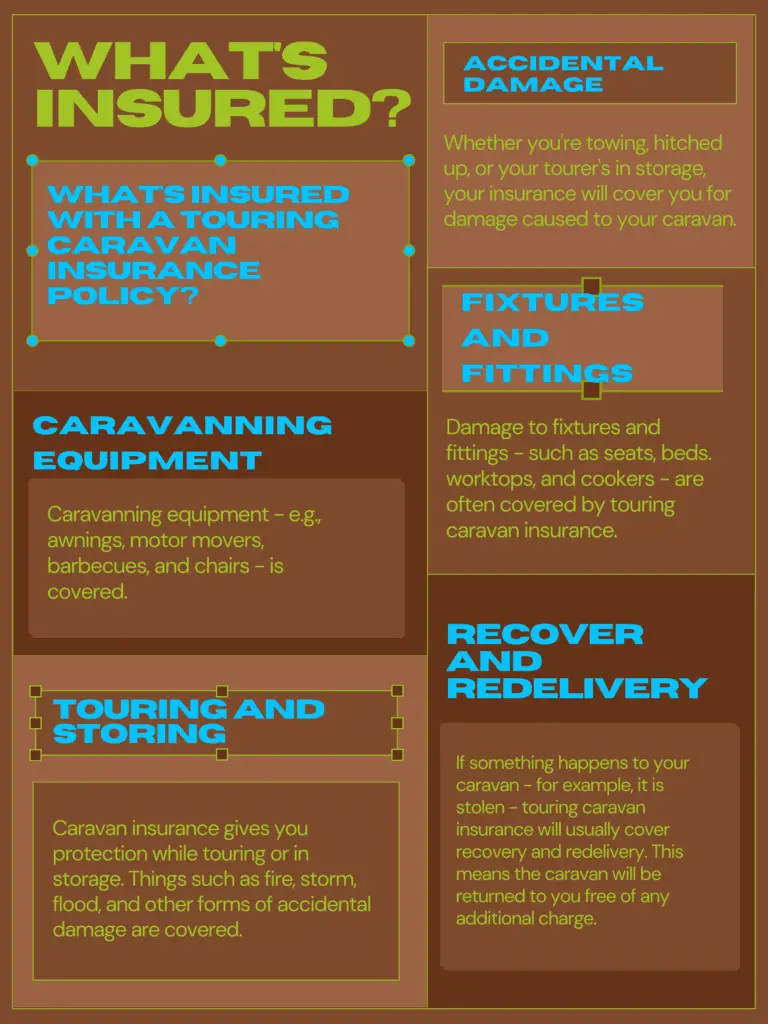

Caravan insurance covers your caravanning equipment — e.g., awnings, motor movers, and barbecues — fire, theft, storm, flood, and accidental damage, and damage caused to the caravan while you’re towing it, pitched up or storing it.

Depending on the insurer you choose — which will affect what’s covered and what isn’t — caravan insurance tends to be fairly comprehensive. In this blog post, I’ll give you a more in-depth answer to the question — including some comments from one of the UK’s top caravan insurance companies — and also explain what isn’t covered by touring caravan insurance.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

What Does Caravan Insurance Cover?

What your insurance covers will depend on several factors, such as:

- The insurer

- The policy type

However, we spoke to Liz Harrison — PR & Communications Manager at leading touring caravan insurer Caravan Guard — as part of our Q&A — which you can read in full by clicking here. As part of that interview, we had the opportunity to ask Liz what caravan insurance covers. Here’s what she said.

“A specialist caravan insurance policy like ours will cover your caravanning equipment, such as expensive awnings, a motor mover and also TVs, barbecues, chairs etc, that you use with the caravan.

“Caravan insurance gives you protection whilst touring or in storage, for things like fire, theft, storm, flood, and accidental damage.

“Caravan insurance will also cover you for damage caused to the caravan whether that’s whilst towing, when pitched up, or in storage. Plus, it covers fixed fixtures and fittings in your caravan such as seats, beds, worktops, cookers, and shower trays if damaged, as well as ‘Caravan Equipment’, which includes things such as Aquarolls and security devices, and any items which are used solely in the caravan, such as televisions or radios.”

While the above is Caravan Guard-specific, the same applies to the majority of caravan insurers. I spoke to a few insurers while researching the blog post and many said similar to the comments above from Caravan Guard.

Everything included on the infographic above is what’s covered by your typical touring caravan insurance policy. However, what’s insured will differ from policy to policy. For example, some insurance policies will be more comprehensive.

Some touring caravan insurance policies will also include:

- European cover

- Equipment replacement

- Emergency accommodation

- Protected no claims discount

Obviously, the more you have insured the greater your insurance premium will be. I actually wrote an article — How Much Is Touring Caravan Insurance Roughly? — that contains research into how much touring caravan insurance costs. To give you a rough idea, caravan insurance can cost as little as £90 but as much as £500 upwards. I explain in much more detail in the blog post mentioned, so it’s well worth a read if you’re currently looking to insure your tourer.

This brings us onto the question of what isn’t covered by touring caravan insurance. Let’s have a look at some of the things that aren’t typically insured by a touring caravan policy.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

What’s Not Covered By Caravan Insurance?

With any insurance policy, there are exclusions — things that aren’t insured by the policy. Touring caravan insurance is no different.

Typically, the following are not insured by caravan cover:

- High-risk items: High-risk items are usually defined as small, valuable items that can be stolen easily. A few examples of items that could be defined as high risk include mobile phones, jewelry, antiques, and anything made of valuable materials (i.e., gold, silver, and other precious metals)

- Usage for purposes not covered in the policy: If you’ve told your insurer that you’re using your caravan for personal/family use and you decide to use it for business, your insurance is invalid for as long as you’re using it for purposes not covered in the policy

- Mechanical and electrical breakdown: If something mechanical or electrical breaks down, the costs of repair/replacement are not usually covered by touring caravan insurance. You should ensure the maintenance of anything mechanical and electrical as part of your obligation to keep your caravan roadworthy

- Depreciation/wear and tear/gradual deterioration: As your caravan ages, wear and tear and deterioration are natural occurrences you can do nothing about. Anything linked to wear and tear/natural deterioration is unlikely to be covered by your policy

- Theft where you have not complied with security/storage requirements, or where all the security devices you’ve said you use are not used: If you do not comply with security and storage requirements, or you’re not using the security devices you’ve told your insurer you use, you’re not covered if your caravan is stolen. Be honest with your insurer and make sure you use all the security devices you say you’re going to

- Damage caused by domestic animals: Damage caused by domestic animals — including biting, chewing, scratching, and tearing — is not usually covered by caravan insurance. It’s always a good idea to avoid bringing any pets that have a history of causing damage!

- Legal expenses cover: Legal expenses cover is not included as standard in touring caravan insurance. However, it is often available for an extra fee if you think it’s worth the investment

Some of the above — such as legal expenses — are covered with certain policies which may result in an extra charge. And other things that aren’t covered by caravan insurance can be covered by other types of insurance — e.g., mobile phone insurance for mobile phones.

Alongside everything above, there are some other obvious exemptions. For example, if your insurance company deems you (or another occupant of the caravan) guilty of malicious damage or theft, your cover will be invalid. That really goes without saying.

Specialist cover for folding campers and trailer tents. Caravan Guard gives you cover for storm, theft, accidental damage or vandalism under their touring caravan insurance policy. Get a quote today.

Anyway, I hope that you’ve found this blog post useful. If you’re currently researching caravan insurance, Folding Camper World has published several blog posts that you might find useful. Here are just a few particularly handy posts:

- What Is New For Old Caravan Cover? In this blog post, I explain what New for Old caravan insurance is. I also give some premium examples to show how the two types of insurance — New for Old and Market Value — differ cost-wise.

- How Much Is Touring Caravan Insurance Roughly? Wondering how much touring caravan insurance is going to cost you? We got quotes for 6 different caravans in 3 different categories (low end, mid-range, and high end) to work out an average insurance premium.

- Tips For Reducing Your Caravan Insurance Premium. Caravan insurance can be very expensive. In this blog post, we explain how you can reduce your premium and save some money.